Is the 60/40 Portfolio Still Alive in 2025?

According to Morningstar, the classic 60/40 portfolio of US stocks and bonds fell more than 16% in 2022—its sharpest drop since 2008. But the deeper story is that this wasn’t just a bad year. From 2021 to mid-2023, the 60/40 strategy delivered its worst stretch of underperformance in 150 years, driven largely by bond losses during a period of aggressive rate hikes and inflation. For many investors, this broke a fundamental assumption: that bonds reliably cushion equity downturns. But in a high-inflation, rising-rate environment, both asset classes sank together. So is the 60/40 portfolio dead in 2025—or just due for reinvention?

The article unpacks why the strategy may still have value, when it breaks down, and how it’s being adapted in today’s volatile market.

Key Takeaways

- The classic 60/40 mix suffered a historic drawdown in 2022 due to inflation and rate shocks.

- The strategy may still work—but only if assumptions about bonds, diversification, and risk are updated.

- Some investors are adding alternatives, international exposure, or factor tilts to adapt.

- Behavioral discipline matters more than precise allocation models.

- Tools like diversification scoring or stress-test modeling can help assess durability in today's market.

Why the 60/40 Broke Down

The 60/40 portfolio—60% equities, 40% fixed income—has long been a default for balanced investing. Historically, bonds offered income and stability during stock selloffs. That inverse relationship worked well in decades when inflation was low and rates trended downward.

World Economic Forum analysis shows the Fed’s rate hikes from March to December 2022 were the steepest in over 30 years—nearly twice the pace of the 1988–89 tightening cycle. Inflation peaked above 9% (BLS, 2022). As a result, bond prices fell sharply, alongside equity markets. The two pillars of the 60/40 both cracked.

This revealed a key vulnerability: correlation risk. When markets are hit by a macro shock—like inflation—diversification can break down. Bonds may no longer be the counterweight many assume they are.

So what happens to a model that assumes they are?

- Hypothetical: Imagine a 38-year-old investor rebalancing quarterly into a 60/40 mix through 2022. As both assets drop, the rebalancing buys into weakness—but without the usual bond support. The loss compounds, and the investor begins questioning the entire strategy.

For some, this was a wake-up call that asset allocation models need to reflect the macro regime, not just historical averages.

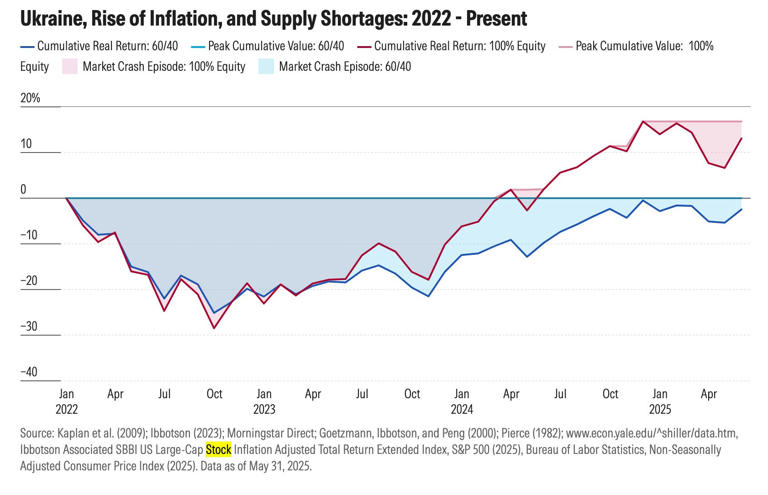

The chart below illustrates how both equities and bonds suffered simultaneously through 2022–2023, challenging the assumption that bonds act as reliable ballast in diversified portfolios.

It's Not Dead—Just Dated

Despite its challenges, the 60/40 portfolio isn't obsolete. But it's no longer one-size-fits-all. The real question isn't whether the strategy works, but under what conditions.

- When inflation is stable and rates are predictable, 60/40 may still offer a reasonable balance of growth and protection.

- When inflation is volatile or negative correlations break down, the mix can underperform.

Some investors are adapting with modest changes:

- Adding Treasury Inflation-Protected Securities (TIPS) to hedge real rate risk

- Including commodities or real assets for inflation exposure

- Diversifying globally to capture growth beyond the U.S.

- Using factor strategies like low volatility or value tilt

The point isn’t to throw out the framework. It’s to reexamine the assumptions that once made it work.

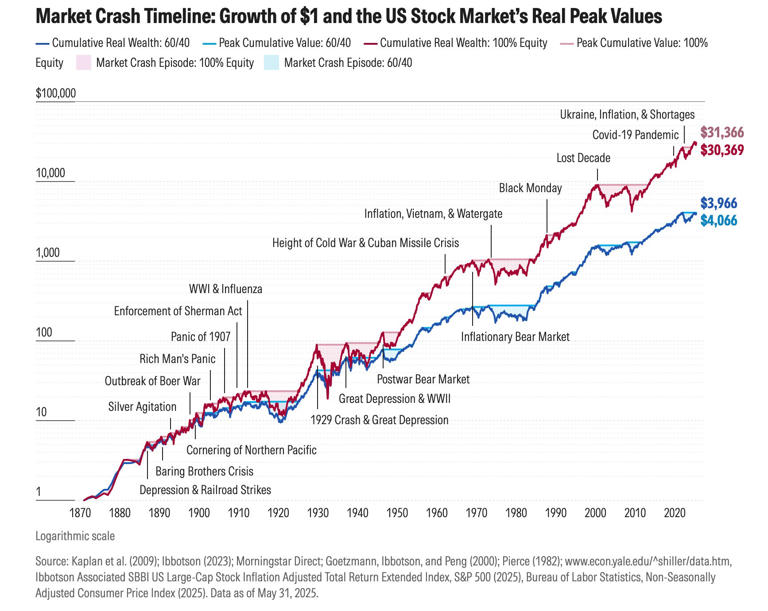

Despite short-term pain, the long arc of history still favors diversified strategies. The chart below shows how both 60/40 and 100% equity portfolios have delivered substantial long-term gains—even through wars, inflationary shocks, and recessions.

Still, the recent divergence highlights why investors are questioning whether past models still apply in the current macro regime.

Behavior Still Matters More Than Models

In practice, allocation discipline often matters more than allocation precision. During drawdowns, many investors panic-sell—locking in losses and derailing long-term plans. A diversified strategy like 60/40 only works if followed consistently.

That makes behavioral compatibility a feature, not a flaw. Even if 60/40 isn’t optimal on paper, it may be optimal for investors who need simplicity and consistency. Similarly, the cost of complexity—chasing tactical changes, adding too many asset classes, or timing macro trends—can often outweigh the gains.

Put differently: the best strategy is one that’s durable under pressure.

How to Stress-Test It

Some investors are now evaluating portfolios less by historical returns and more by scenario durability. In this framework, tools like:

- Diversification scoring (how uncorrelated assets actually behave)

- Historical drawdown simulations (how portfolios performed in stress years like 2008 or 2022)

- Forward-looking scenario modeling (how inflation or rate shocks affect real returns)

can help assess whether a portfolio’s mix is built to endure shocks.

Chasing the perfect allocation is a distraction. Rebalancing within an imperfect, but behaviorally sustainable, strategy is more likely to succeed long-term.

How optimized is your portfolio?

PortfolioPilot is used by over 30,000 individuals in the US & Canada to analyze their portfolios of over $30 billion1. Discover your portfolio score now:

Analyze your entire net worth

360° portfolio analysis, AI Assistant, and personalized recommendations guided by our Economic Insights Engine.

Global Predictions provides investment advice only through its internet-based application, PortfolioPilot, and only to individuals who are advisory clients of Global Predictions pursuant to written advisory Client Agreements ("Advisory Services"). The publicly available portions of the Platform (i.e., the sections of the Platform that are available to individuals who are not party to a Client Agreement - including globalpredictions.com and portions of portfoliopilot.com) are provided for educational purposes only and are not intended to provide legal, tax, or financial planning advice. To the extent that any of the content published on publicly available portions of the Platform may be deemed to be investment advice, such information is impersonal and not tailored to the investment needs of any specific person. Nothing on the publicly available portions of the Platform should be construed as a solicitation or offer, or recommendation, to buy or sell any security. All charts, figures, and graphs on the publicly available websites are for illustrative purposes only. Before investing, you should consider whether any investment, investment strategy, security, other asset, or related transaction is appropriate for you based on your personal investment objectives, financial circumstances, and risk tolerance. You are also encouraged to consult your legal, tax, or investment professional regarding your specific situation. Registration does not imply a certain level of skill or training. Investing involves risk. The value of your investment will fluctuate, and you may gain or lose money.

The contents of the Platform may contain forward-looking statements that are based on management's beliefs, assumptions, current expectations, estimates, and projections about the financial industry, the economy, or Global Predictions itself. Forward-looking statements are not guarantees of the underlying expected actions or future performance and future results may differ significantly from those anticipated by the forward-looking statements. Therefore, actual results and outcomes may materially differ from what may be expressed or forecasted in such forward-looking statements.

Note: our use of the term AI refers to all artificial intelligence models used including large language models, proprietary economic models that incorporate regression or dynamic factors, and machine learning methods like supervised learning.

2. As of February 20, 2025

3. $30B Assets on Platform as of February 20, 2025. Aggregated across all plans (including the free plan). Assets on Platform represent the total value of connected and manually inputted accounts (including assets like real estate and private equity) and does not in any way represent Asset Under Management as Global Predictions does not manage any client funds.

8. Case studies presented are hypothetical scenarios and intended for illustrative purposes only. They do not represent an actual client, investment or experience, but rather are meant to provide an example of the intended investment process and methodology. An individual's experience may vary based on his or her circumstances. There can be no assurance that the Firm will be able to achieve similar results in comparable situations. No portion of this case study is to be interpreted as a testimonial or endorsement of the Firm's investment advisory services. The information contained herein should not be construed as personal investment advice.